Satoshi published the whitepaper on 10/31/2008. Right at the moment of peak despair during the 2008 financial crisis. Trust had been lost in a world that ran on trust.

But why October 31st? Why that date specifically? It certainly wasn’t because Satoshi was a fan of halloween, it must have had a deeper meaning. With all of his actions, Satoshi demonstrated a careful precision.

Satoshi had been working on Bitcoin for at least a year and a half before publishing the whitepaper.

“I believe I've worked through all those little details over the last year and a half while coding it, and there were a lot of them. The functional details are not covered in the paper, but the sourcecode is coming soon” - Satoshi Nakamoto

On August 18, 2008 Satoshi registers registers Bitcoin.org through anonymousspeech.com.

Satoshi was ready and waiting to hit the send button throughout 2008. What was so special about October 31st?

Out with the old, in with the new

I believe that Satoshi published the Bitcoin white paper on 10/31 as a hat tip to the ancient Gaelic festival of “Samhain” which was also the date in which Martin Luther nailed his 95 Theses to a church door. Both represent an end of the old and the beginning of the new.

Samhain represented the end of harvest season and the beginning of winter.

The early Catholic church, in an attempt to gain believers, adopted some of the festivals such as Samhain, and in 835 created “All Saints Day” to coincide on 10/31. This is what we call “Halloween” or “All hallows’ eve” a major holiday in the Catholic world.

On October 31, 1517 Martin Luther nailed his 95 Theses onto the doors of the Castle Church (dedicated to All Saints). Luther was outraged by the idea that sinners would be able to reduce their sins through payments or unpaid work. Under the Pope, these were considered part of the church treasury, which allowed those in power to continue their lavish lifestyle at the expense of the masses. Luther undermined the authority of the Pope through his 95 Theses, starting a process of reformation. Luther’s ideas became very popular, spreading around the world through the newly invented printing press changing the course of the world forever.

Similarly, Satoshi was outraged at the massive breach of trust by existing financial institutions:

“The root problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust. Banks must be trusted to hold our money and transfer it electronically, but they lend it out in waves of credit bubbles with barely a fraction in reserve.” — Satoshi Nakamoto

Satoshi used 40 years’ worth of technological advancements and combined them to create Bitcoin. Bitcoin’s blockchain enabled it to be accessible and transmittable to anyone in the world, just as the printing press enabled the spread of Martin Luther’s ideas.

Both Satoshi and Luther carefully chose October 31st to announce their ideas, symbolizing death and renewal. Both saw the imprisonment of people by these legacy systems and suggested ousting the existing authority as the solution to the problem.

Bitcoin marks the end of fiat and the beginning of a new monetary standard. Let us go forth boldly, and build a new world.

“The present is theirs; the future, for which I really worked, is mine.” - Nikola Tesla

HODL,

Dan

Bitcoin’s future has been radically altered in the past 18 months.

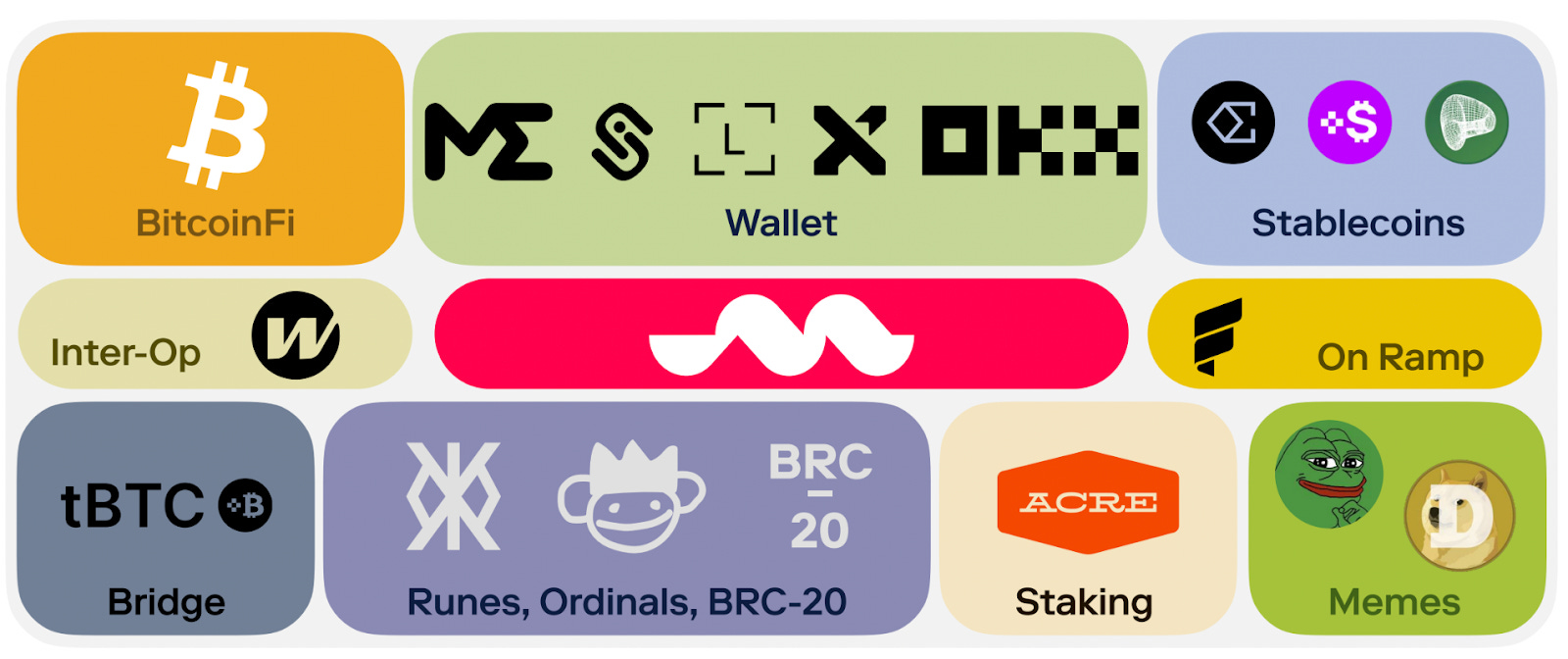

Some people call this period the “orange wave” or “Bitcoin Season 2” or even the “Bitcoin Renaissance.” All these names refer to one thing: an explosion of development, investment, and utility and broader attention paid to the Bitcoin brand and ecosystem. What started with inscriptions and runes has spilled over to new offchain products, onchain scaling solutions, and more.

In this new era of Bitcoin history, a unique approach to scaling the Bitcoin-native economy has been in development since early 2023. Called the Spiderchain, this protocol being developed by Botanix Labs is defined by its focus on simplicity and security while following an ambitious roadmap with the singular goal of supporting a decentralized financial system running on Bitcoin.

Most readers of this newsletter may have never heard of the Spiderchain let alone know what they can do with it. The purpose of this note is to answer both of those questions, so keep reading.

The Basics of Bitcoin’s Spiderchain

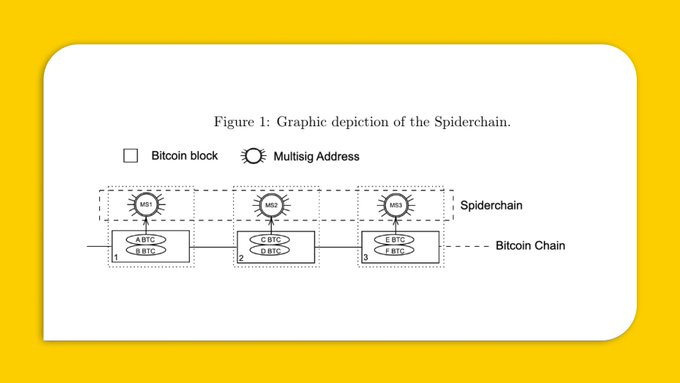

In short, the Spiderchain is a new primitive network for rapidly expanding the simplicity, security and scalability of a second-layer ecosystem built directly on Bitcoin. A series of successive, randomized and decentralized multisigs secure all assets moved from the Bitcoin base layer. Every Bitcoin block is associated with a new multisig created between a set of random participants (called Orchestrators) from the Spiderchain. This growing chain of multisigs can be seen as a sort of web that safeguards all bitcoins moved to the Spiderchain.

A key facet of the Spiderchain primitive is the ability to bring the Ethereum Virtual Machine (EVM) software layer to the Bitcoin ecosystem. Bitcoin – a monetary protocol – is universally recognized for its strong Lindy Effect that strengthens with each new block. Similarly, the EVM is a Lindy software layer that supports billions of dollars in capital, millions of users, and thousands of applications. But the problem is all of this exists on the wrong blockchain – it should be on Bitcoin. Bringing all the EVM-based liquidity, users, applications, and developers to the EVM-equivalent layer on Bitcoin (i.e., the Spiderchain) will have a powerful growth effect for Bitcoin.

From the opening to the whitepaper by Botanix Labs, the Spiderchain’s purpose is described as:

“With Bitcoin as the most decentralized and secure bottom layer, the second layer will open the doors to the composability, ecosystem and capabilities of Ethereum smart contracts.”

The Spiderchain also introduces an encryption system that is novel to the world of cryptocurrency but old hat to the world of cryptography – forward security. Being forward secure means that participating users in a network can refresh their keys across epochs (i.e., new sets of randomized multisigs with each block) in a way that any instance of compromise that threatens the current secret keys leaves all prior encrypted keys secure. If Block 100 is compromised, for example, Blocks 1 through 99 are unaffected. This is a powerful tool for any cryptocurrency network but especially for a second-layer protocol because security actually is a higher priority on a Layer 2 compared to the base layer (but that’s a topic for another article).

Sharing his own thoughts on security and the Spiderchain, Jameson Lopp published a blog article that concluded with:

“At a high level, I think that Spiderchain make sense when the conditions are as described in the whitepaper. The million bitcoin question is how well the system can hold up to edge cases and adversarial conditions.

Scaling Bitcoin and building a robust Bitcoin-native decentralized finance (DeFi) ecosystem has been a challenge for many years. Part of the reason for the idea of the Spiderchain was to avoid creating something completely new and instead to adopt something the market already uses and is familiar with (e.g., the EVM) and bring those network effects to Bitcoin. What makes this even better is that the Spiderchain can run on Bitcoin Core as it exists today – no new token is needed, no new BIP is needed, no other blockchain is needed.

In a blog post that shares an overview of the purpose of the Spiderchain, the Bitfinex team wrote:

“The primary motivation behind Spiderchains is the significant growth of decentralised finance applications on platforms like Ethereum, which are largely absent on Bitcoin.”

But this begs the question, “What can you do on the Spiderchain?”

What Can You Build on the Spiderchain?

The short answer to this question is anything that has been built on Ethereum or any Ethereum layers can be quickly copy-pasted to run on the Bitcoin-native EVM layer being built by Botanix Labs. In fact, any application that finds demand from users outside of Bitcoin should be brought back to run on Bitcoin. That’s the vision for the Spiderchain. Bitcoin should eat everything.

The longer answer comes with some examples. Bitzy, for example, is a Spiderchain-native decentralized exchange platform for Bitcoin users to engage in markets for other assets without having to leave Bitcoin for another blockchain. Vertex is another trading platform that has deployed on several other networks outside of Bitcoin, and now they are coming to Bitcoin through the Spiderchain.

Beyond these two examples, there are collectibles, staking protocols, stablecoins, and much more that are in development and testing on the Spiderchain testnet. For more information as the progress continues, join the Botanix Labs team on X or Discord.

]]>